The SaaSpocalypse? Why Usage, Outcomes, and Expertise Mean SaaS Is Far From Dead

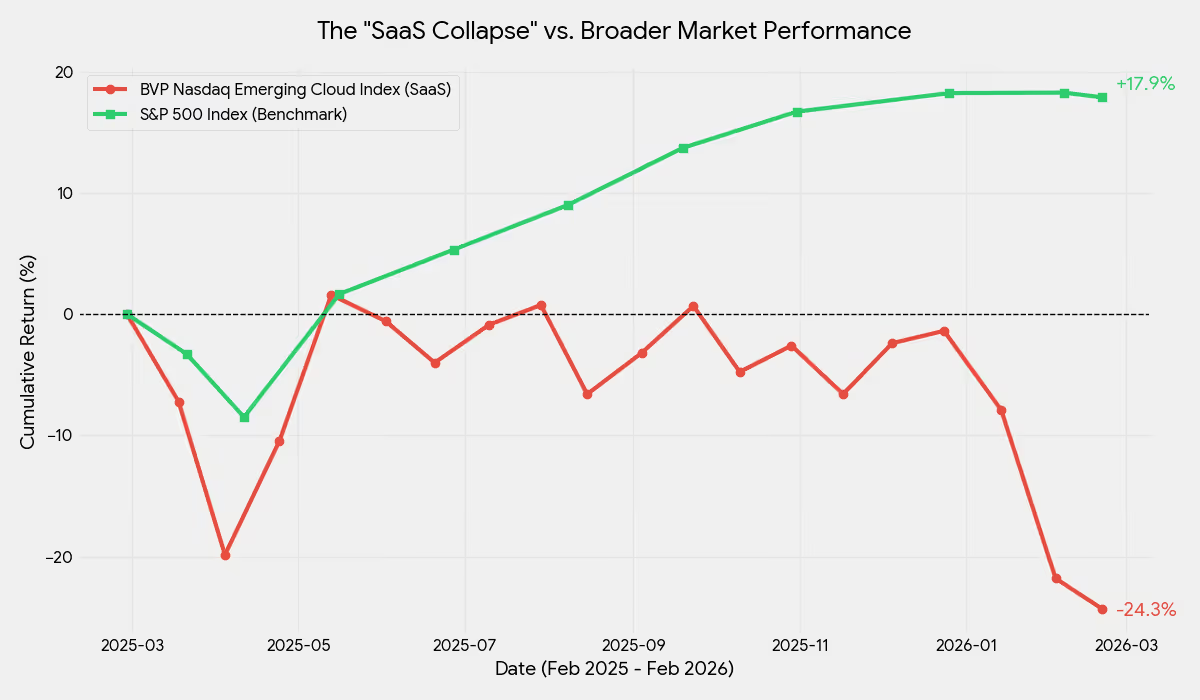

Early 2026: software stocks take a historic dive, wiping out nearly $1 trillion of market cap on fears that AI (especially agentic plugins, no-code bots, and automated workflows) will compress the core value of SaaS. “SaaSpocalypse” is trending everywhere as doomsayers proclaim that classic SaaS, and its dominant per-seat model, is finished.

No question, AI agents and automation are upending familiar business models. Large incumbents find core “per seat” growth slowing as customers question why they should pay for licenses when AI handles what used to take a room of knowledge workers. Investors, spooked by workflow automation and the speed of AI-first startups, are betting against the model they loved for two decades.

But here’s what I see: SaaS isn’t dying. It’s evolving and the quickest learners, far from being doomed, if they adapt their business models and technology, can emerge even stronger.

SaaS: Still Sticky, Trusted, and Cash-Generating

Despite the headlines, consider these facts:

- Global SaaS spending is projected to grow from $313B to $500B by 2028. The subscription model, the engine of predictable cash flows, customer relationships, and high gross margins, isn’t vanishing overnight.

- Incumbents like Salesforce, ServiceNow, and Microsoft enjoy massive moats: integrations, compliance, and years of customer trust. Switching costs in core business operations are real. Businesses prefer risk-managed, enterprise-grade vendors for AI as much as they do for CRM or ERP.

- SaaS isn’t just technical code. It’s expertise, workflow, data hygiene, and support: elements that aren’t easily “deployed” by the latest LLM plugin.

Ignore the False Parallel: Siebel’s Fall vs. The “Rise of Salesforce”

One argument making the rounds compares today’s upheaval to the legendary disruption of Siebel (where I was a senior operating executive) by Salesforce. Back then, Siebel (history lesson for "young uns" -- Siebel was an on-premise, perpetual license software company that created the CRM category and went from $2M to $2B in revenue in less than 5 years) was unable to respond effectively to the “no software” revolution: multi-tenant cloud architecture, subscription pricing, and a new category narrative. Salesforce’s swift rise wasn’t just about technology; it was a full-stack business model and go-to-market innovation: a classic case of an inflexible incumbent business model and technology (Siebel) overtaken by a fundamentally new delivery and revenue model designed for scale, openness, and ongoing customer success (Salesforce).

Today, some argue that “AI-native” companies are poised to do the same to the SaaS giants. But this analogy doesn’t hold up for me. Why? AI is a powerful new driver but doesn’t (by itself) upend the operating system of trusted, interoperable, expert-supported software. In fact, many of the “AI-native” products rely on the same cloud pipes, enterprise integrations, subscription pricing (often usage-tiered!), and customer support playbooks as the “old guard.” The step change isn’t as dramatic as Siebel to Salesforce; it’s evolutionary, not revolutionary.

The “Per Seat” Squeeze—And the Strategic Response

Despite what I just wrote, the concern is real: AI copilots and workflow agents take on more tasks for fewer human “seats.” That means fewer paid licenses, especially for routine, horizontal features. Venture and public investors noticed, pricing stocks accordingly.

But the best SaaS companies aren’t standing still. Here’s how they’re adapting, as documented by Bain, Forrester, and industry insiders:

1. Usage and Outcomes-Based Pricing

- Current SaaS providers are already moving away from pure seat licensing to usage (how much data you process, how many calls/tasks you run) and outcome-based agreements (charging by value delivered—e.g., qualified leads, closed deals, or efficiency gains). Companies like HubSpot, Zendesk, and Salesforce have piloted usage-based AI tiers, billing customers for “AI credits,” number of automations run, or tangible outcome metrics.

- Customer benefits: can better align their costs with realized value, reducing upfront risks and improving renewal rates.

- Vendor benefits: get rewarded for customers’ success, can cross-sell upmarket, and can preserve or even expand wallet share as AI drives new value.

"Contracts now include hybrid terms—minimum subscriptions plus variable usage or success-based add-ons. The highest NPS comes from customers who feel vendor incentives are aligned with their business—not license maximization." Forrester Research

2. Subscription with Embedded AI

- Companies are launching “AI-enhanced” subscription plans instead of forcing customers to drop legacy modules. This hybrid model soothes buyer anxiety and channels adoption through trusted platforms.

Subscription is the delivery vehicle. The differentiation is now: do you deliver AI-enabled outcomes reliably at scale, not simply X seats per month?” Bain Consulting

- Newer SaaS-born startups (including “AI-native” platforms) are still using recurring contracts: proving the model isn’t dead, but the offering is shifting toward value and flexibility.

The Expertise Moat—the Lasting Defense

With AI eroding traditional technical and data moats, domain expertise, integration, and client trust are rising in value:

- Vendors with deep workflow understanding, strong vertical knowledge, and compliance DNA are building “expertise moats”: embedding institutional know-how into both their products and the prompts, guardrails, and data models that drive their AI features.

- The interplay of expert intuition, curated best practices, and operational support is something generic AI can’t easily displace.

- Vertical SaaS, regulated domains, and platforms that support highly-specific processes (healthcare, logistics, finance) are resilient, as these require ongoing adaptation, judgment, and risk management.

Adaptation, Not Apocalypse

Yes, SaaS companies that cling to legacy seat licensing for low-value, commodity features are at risk. But those that:

- Continuously embed AI in their products

- Offer usage/outcomes-based pricing aligned with customer value

- Double down on their expertise, workflow DNA, and integration moat will continue as “central nervous systems” for the enterprise.

The panic is warranted...for laggards. But from my cheap seat, the future is abundant for SaaS innovators who evolve their delivery and business models. The subscription isn’t outdated: it’s just being refocused on value, not headcount.

Bottom line: In my opinion, SaaS isn’t dead. It’s being reborn. The best companies are switching from “we sell seats” to “we deliver outcomes, powered by our expertise” faster than the market realizes. AI isn’t the SaaSpocalypse: it’s a forcing function for the next evolution.

More than 90% of all VC-backed startups fail outright. Up to 60% of all new products launched by enterprises fail to achieve traction. Traction Gap Partners is a "Market Engineering Studio". Our website is tractiongappartnersdotcom .